Stocks. Compound interest. S&P 500 index fund.

If you’re already bored and disinterested after reading that first line, then this post isn’t for you.

There are no easy get rich secrets, magic tools, or sales pitches for shitty products here.

You’re not going to learn how to turn 100 dollars into $1,000 in a day, or become a stockmarket millionaire overnight.

The world has enough scam artists claiming they can help you do that. So if you want to get conned and commit financial suicide, feel free to search for those individuals.

Now… if you want to learn how to invest money to get good returns for retirement, keep reading.

You’re about to discover an investment strategy that’s as exciting as a tree stump. It’s boring, unsexy, slow, and painfully simple.

But the reality is, it works extremely well.

It’s one of the strategies that smart investors use to create ridiculous amounts of wealth.

I’m talking about: the power of compound interest.

And today you’re going to learn how it can help you create your own wealth.

But before you do that, let me tell you a bit about compound interest.

How Compound Interest Works?

Compound interest is basically a percentage of money you earn on both your initial deposit and the money you continue making as a result of interest earned.

For example, if you invest $100 for 5 years and your annual compound interest rate is 7%, this is what you’d earn:

Year 1 would be $100 x 7% = $105

Year 2 would be $107 x 7% = $114.49

Year 3 would be $114.49 x 7% = $122.50

Year 4 would be $122.50 x 7% = $131.08

Year 5 would be $131.08 x 7% = $140.26

The example above is basically showing you that you’re earning interest on your interest.

If it all sounds confusing, then think of it this way:

Imagine you’re standing at the top of Mount Everest with a tiny pebble (your initial deposit). If you decide to toss that pebble down the mountain side, something crazy is going to happen…

Assuming it doesn’t kill anyone, that pebble will roll down the mountain gathering debris (interest) until it reaches the bottom as an amazingly large boulder (total compounded earnings).

Make sense now?

How This Applies to You

As I said before, this strategy has created amazing wealth for millionaires and billionaires. It’s also the strategy I use as well.

BTW, in case you’re wondering, I’m not a millionaire (yet). My net worth puts somewhere in the upper middle-class of Americans.

None of that matters though. What matters is how I got there. So keep reading to find out exactly what I’ve done – and continue to do – to build wealth.

Obviously this isn’t financial advice nor am I fattening you up for a sale. I’m just sharing a strategy I copied from rich people, to show you what’s possible. Whatever you do with this information is your business.

You see, when it comes to making money, everyone wants “easy step-by-step instructions” they can use themselves.

The good news is, what I’m about to show you is easy and it works.

The bad news is, it’s not quick and it ain’t sexy.

This stuff is so boring that I’m just glad you’re still reading about it.

How to Turn Money into More Money Fast but Slow

I know what you’re thinking, “That’s ridiculous, you can’t do something fast but slow.”

My response to that is… of course you can!

Here’s how:

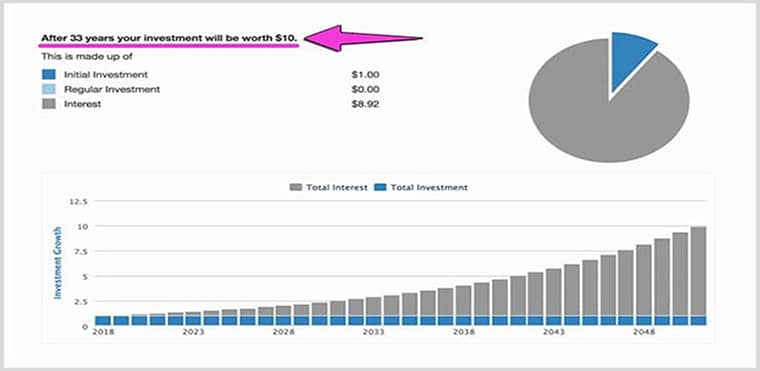

Imagine for a second that you’re in your early 20s with a crisp $1 bill burning a hole in your pocket.

But instead of balling out with your dollar, you decide to invest it in an S&P 500 index fund. And let’s assume that index fund historically performs at 7.2% (adjusted for inflation) per year.

If you do nothing else but leave your dollar alone and reinvest all the interest it accumulates, something amazing will happen…

In just three decades, that $1 will be worth $10. #compoundinterestFTW

Here’s a chart for illustration:

Oh dear, I can hear the alarms going off in your head and the critics coming out of the woodwork like cockroaches. But hang on a sec…

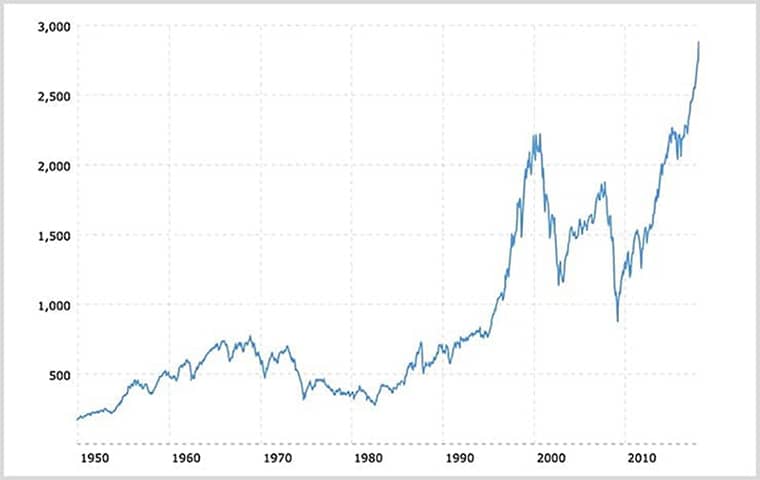

What I just told you isn’t a pile of poo. It’s actually based on factual data regarding the historical returns from the stock market.

Just look at this S&P historic chart:

As you can see from the chart above, this is very real.

And now that you know I’m not blowing smoke up your ass, let me tell you how I approach this.

For every $1 that I have, I see it as being worth 10-times more to me in 30 years (aka – retirement).

For example, that hot new $900 Smart TV is worth $9,000 to me in the future. Those cool $100 runners, they’ll be worth $1,000 to me in thirty years.

So the question I usually ask myself is…

Self, would you rather have that cool tv now or $9,000 in 30 years when you need it?

That’s the kind of mindset I have when it comes to money.

Now, I’m not saying you need to be frugal to the point you don’t enjoy life.

What I’m suggesting here is that you try to imagine the future value of something decades from now. That way, you’ll have an idea of what it’s going to cost you later on.

It’s funny because you can apply this to more than just money. It can work for relationships, health, and other areas of your life. But I digress.

By now your mind should have a clear idea of how this investment strategy works using the power of compound interest.

If you’re still lost, go take a shot walk then come back and read this post again.

Like I said, this strategy isn’t complex or scary. In fact, the concept can be broken down into what some call the “Three I’s” of investing, which are:

- Invest early

- Invest frequently

- Invest for the long-term

If you remember those things when it comes to investing your money, your future self will thank you for doing so.

But, but…if it’s so simple why isn’t everyone doing it?

Good question. Maybe it’s the same reason why so many people don’t go to the gym.

Too vague? Okay. Let me tell you…

Why most People Don’t Invest like This

The reason people don’t invest their money like this isn’t because of a lack of information. After all, there’s a ton of free resources out there – this site is one of them.

The best answer I can give you as to why they don’t do it is:

Most people find it hard to do simple things because their desire for instant gratification overpowers all logical thought.

For instance, people know that exercise and dieting are the only guaranteed ways to lose weight naturally. Yet they scramble to buy the next weight loss pill, fitness accessory, or trending diet on the market.

Why? Because those things promise easy, fast, and instantaneous results. As opposed to diet and exercise, which is a long-term process.

The same thing applies to investing. Everyone wants an easy step-by-step guide to make 100k, turn 500 dollars into 1000, or turn 10k into 1 million.

But having the discipline to invest money and leave it alone for 10, 20, or more than 30 years, is hard.

So while most people will understand the investment strategy discussed in this post, they just won’t do it. Even if all it takes is just $1.

They’d much rather put that dollar towards things that give them instant gratification right now. Or worse, waste it on shady financial products that promise quick returns.

Heck, you can even predict some of the excuses people will have. Here are a few:

- Man, 30 years is too damn long (No one said it wasn’t)

- What if the stock market crashes and I lose everything? (What if it doesn’t?)

- Great strategy but I have no money, not everyone is rich (Yet you have internet access)

- Some of us have bills and responsibilities (Gonna have those whether you’re broke or rich)

- But I need money NOW! (Great! Sell stuff you’re not using, cut grass, wash cars, start a business, etc)

- Stocks are too high right now, I’m waiting for a drop (folks felt the same way when the S&P was at $3.25 in 1878)

- What if I die tomorrow? (What if you don’t and you end up living long enough to retire broke?)

I can go on forever but those are some of the most common excuses people will have to this post, investing, and probably life in general. The good news is…

…there’s still time for you to start investing and building your wealth.

So if you’re serious about doing that, keep reading.

How to Invest in the Stock Market

When it comes to investing, there are many ways you can enter the stock market.

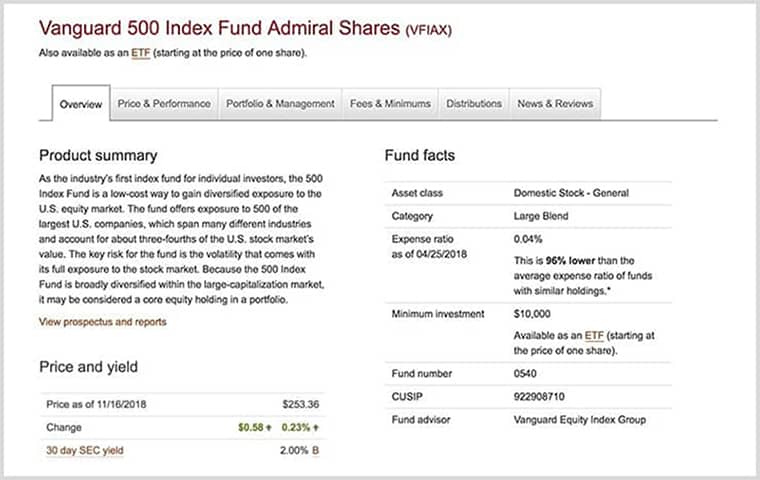

Personally, I invest in the Vanguard 500 Index Fund Admiral Shares (aka VFIAX). It’s a low-cost index fund for individual investors like me who want diversified exposure to the U.S. equity market.

Basically it’s a single fund that invests in 500 of the largest U.S. companies. And by investing in the fund I get access to those companies, which reduces my risk through diversification.

Some of the companies are ones you’ve heard of such as Amazon, Facebook, and Apple. You can see the full list here.

In terms of investment amounts and all that jazz, I keep it simple. Whatever I contribute to my Roth IRA and a 401K accounts, I also add to my VFIAX account. It’s all automated.

And that my dear reader, is my beautifully boring investment strategy in a nutshell. Not that complicated, is it?

Unfortunately, opening this type of Vanguard account requires a minimum invest of $10,000.

If you can afford that, you can get started today.

However, if you’re like me when I first started investing, you don’t have $10,000 lying around. Maybe all you can afford right now is $3.50.

Thankfully, there’s a way you can invest with that amount or even $0.

You can do it with the Robinhood app.

Robinhood has no minimum balance requirements and it doesn’t charge fees on trades. It’s a great way for stock market beginners to get their feet wet.

And along with giving you experience in the stock market, it will also help you build up the discipline you need to make long-term investments.

So if you’re a beginner with limited cash looking to invest in stocks, I definitely recommend using Robinhood.

If you want to give it a try and get a free stock, click here to sign up now.

Eventually you can upgrade to an index fund like Vanguard’s VFIAX when you have the cash to do so.

Final Thoughts About Multiplying Money

Despite what all those people with their sales pitches and fancy financial jargon say, this stuff isn’t complex.

The only reason money and finance seem complex is because they hardly teach anything about it in school.

Plus, you never bothered to expand your knowledge on the subject beyond what you already know.

In reality the concept of investing and using compound interest is simple. I’ve just shown you proof of that.

As I said before, I’m not an expert. All I did was show you how a regular person like me was able to use the same resources that everyone thinks is created exclusively for millionaires.

I didn’t start out with a million dollars, wasn’t born rich, and didn’t inherit or win a ton of money. I started from zero just like most people do.

The truth is…

Learning to be smart with your money takes discipline and self control.

That’s probably going to be your biggest challenge.

You’re going to have to decide if you’re willing to do what most people won’t, so you can live like they never will.

BTW, I’m not saying you shouldn’t enjoy life and do what makes you happy. If a $1,000 Smart TV will put a smile on your face, maybe you should get it.

My only goal is to inspire you to make smarter decisions with your money so you can invest it and earn more in the future.

At the end of the day there’s a fine line between the value something has to you today versus what it could be worth to you in the future.

This is actually my sales pitch to you. I’m trying to sell you on the boring strategy of investing early, frequently, and for the long-term.

Maybe this post isn’t as sexy or mind-blowing as some would like it to be, but it’s real and honest. So if you can appreciate that, then you’re who it was meant for.

There’s also a good chance that you know someone else who would definitely find this post to be helpful. If so, please share it with them. You can do that by clicking the buttons below now.